This is Alpha, the first-born, when he was 2YO.

This is Alpha, the first-born, when he was 2YO. This is Beta, the second-born, when he was about 2YO.

This is Beta, the second-born, when he was about 2YO. This is Gamma, the third-born, when he was about 18MO.

This is Gamma, the third-born, when he was about 18MO.

Bill Delay

Nov

19

2012

I received a bill from a medical facility. Along with the bill was this letter, which was trying to explain why the bill was sent about 3 months after the procedure:

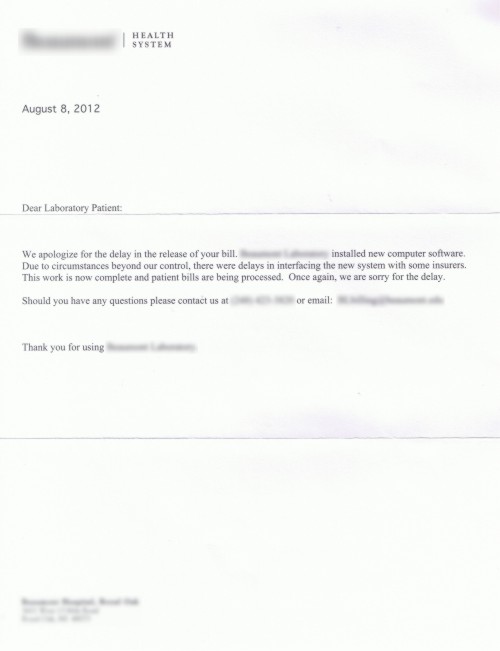

Text of the letter:

Dear Laboratory Patient:

We apologize for the delay in the release of your bill. X installed new computer software. Due to circumstances beyond our control, there were delays in interfacing the new system with some insurers. This work is now complete and patient bills are being processed. Once again, we are sorry for the delay.

Should you have any questions please contact us at XXX-XXX-XXXX or email: x@x.com

Thank you for using X.

I thought about waiting 3 more months, then sending this response along with my payment.

Dear Laboratory:

I apologize for the delay in the release of your payment. I installed new computer software, as opposed to non-computer software. Due to circumstances beyond my control, there were delays in interfacing the new software with my bank account. This work is now complete and invoices are being processed. Once again, I am sorry for the delay.

Should you have any questions, too bad.

Thank you,

Patient

But I didn’t.

For if we had not delayed, surely by now we could have returned twice.

Genesis 43:10